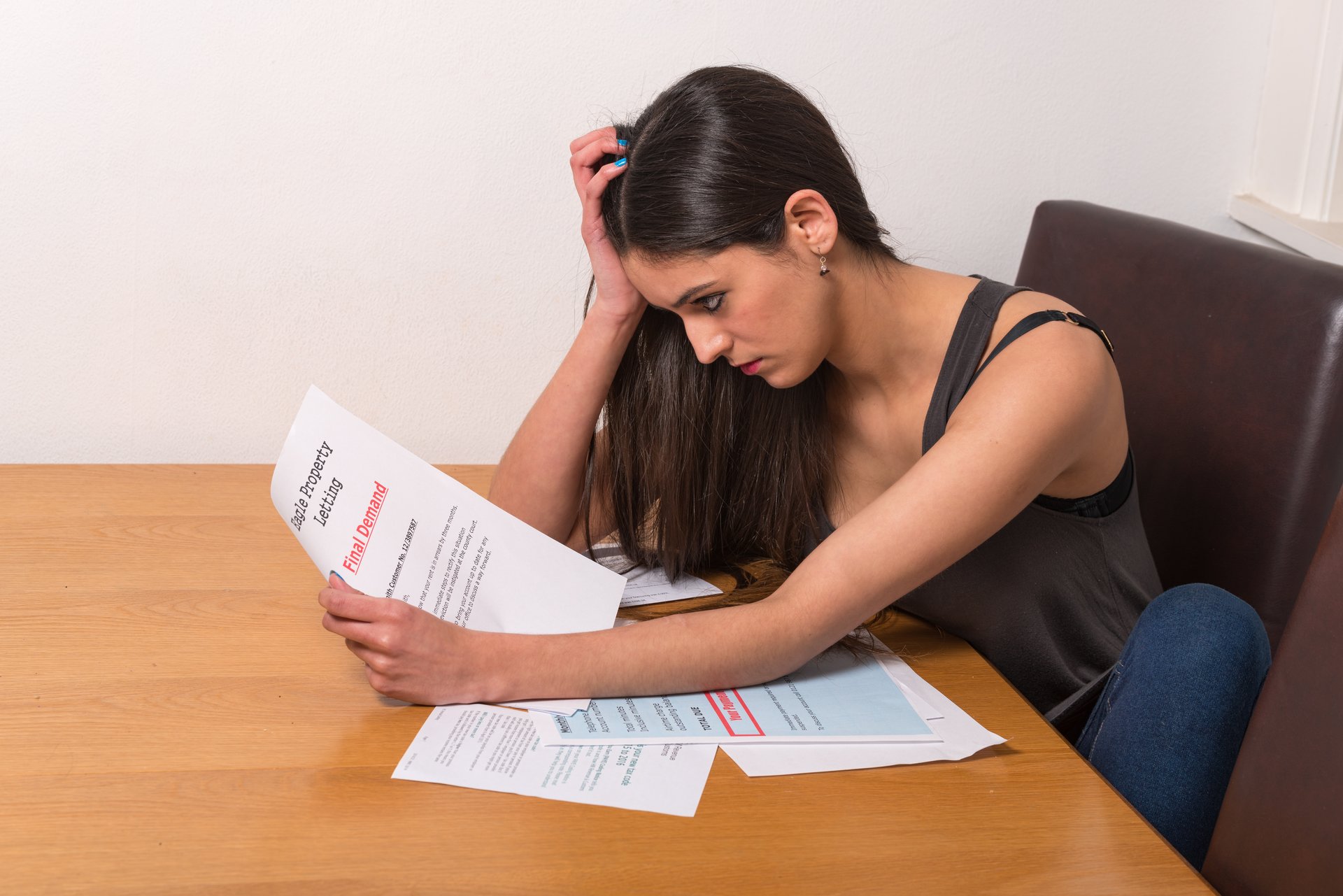

As you’ve probably heard, student loan debt is a problem. Americans now owe more than $1.2 trillion on student loans, more than they collectively owe on credit cards or car loans. Only mortgage debt is higher.

While it may seem that student loans are a problem isolated to students, they affect all of us. Student debt can prevent people from doing the typical things that stimulate our economy, from buying furniture, houses and cars to starting their own businesses.

Which leads us to today’s reader question. It’s about getting out from under student loan debt without having to actually pay it back.

How does someone get student loan forgiveness? — TC

What is student loan debt forgiveness?

As you might imagine, once you borrow money for school, you generally have to pay it back, even if you never attend a class, don’t finish your education, don’t like the education you received, don’t get a job or are unhappy with the loan terms.

But when you have a loan forgiven, canceled or discharged, it means you’re off the hook. Let’s take a look at several methods to eliminate debt. You can learn more about each at this page of StudentAid.ed.gov.

Having student loans canceled, forgiven or discharged

The following is a list of all the ways you can escape student loans. You’ll note that most apply only to loans issued or guaranteed by the government. If your loans are from private lenders, you’ll have fewer options.

Disability discharge: If you have a Direct Loan, Federal Family Education Loan (FFEL) or Federal Perkins Loan, or a loan paid under the TEACH program, it’s possible to have it discharged if you become totally ans permanently disabled.

In order to have a debt discharged, you’ll have to send proof of the disability (such as certification from a doctor) to the U.S. Department of Education. Go here for more information. You can also have the above types of loans discharged by the death of the borrower.

Bankruptcy discharge: You may have heard that you can’t eliminate student loan debt by filing bankruptcy. Not true. While it’s certainly not as easy to eliminate student loan debt through bankruptcy as other types of debt, it does happen. The key is proving “undue hardship.”

You need to meet three conditions to get an undue hardship discharge in bankruptcy, and you’ll need to meet all three. From the StudentAid.ed.gov website:

- If you are forced to repay the loan, you would not be able to maintain a minimal standard of living.

- There is evidence that this hardship will continue for a significant portion of the loan repayment period.

- You made good-faith efforts to repay the loan before filing bankruptcy (usually this means you have been in repayment for a minimum of five years).

As you can see, the bar is set high for those trying to discharge their debt in bankruptcy. But if you think you can meet the requirements, a talk with a bankruptcy lawyer might prove valuable. Read more about this option here.

Closed school discharge: You can get out of Direct Loans, FFEL and Federal Perkins Loans if your school closes and you don’t complete your course of study, or one similar, at another school. There are requirements, like the closure must happen within 120 days of your withdrawal.

If you think you might qualify, check this page of the Federal Student Aid website for details.

School ripoff discharge: While it’s unlikely you’ll encounter fraud or bad information from a community college or university, the odds increase when dealing with for-profit centers of learning.

If your school forges your signature on an application or loan request, your loan was improperly certified, or you were certified as eligible for a profession for which you really weren’t eligible because you weren’t mentally, physically or legally able to do it, you might get your federal student loan discharged.

Teacher loan forgiveness: If you’ve taught full time at a low-income elementary school, secondary school or educational service agency for a minimum of five consecutive years, you might get as much as $17,500 forgiven on Direct Loans or Federal Stafford Loans — whether subsidized or unsubsidized.

Here’s a list of qualifying schools, here’s the application, and here’s the page of StudentAid.ed.gov that explains the details.

You might also get teacher loan forgiveness for Federal Perkins Loans. Check that out here.

Public service forgiveness: Jobs other than teaching might also earn forgiveness on Perkins and other types of loans.

Some members of the military, the Peace Corps and Head Start might qualify, as well as some nurses, law enforcement, and child or family service workers. The amount of forgiveness depends on the type and length of service, type of loan and when it was taken out. Learn more here.

The fastest way to find out if you qualify for forgiveness

As you can see, loan discharge and forgiveness are complicated. The links in this article will take you to information that can help, but if you find your eyes glazing over, try calling your loan servicer. They might be able to tell you in seconds what you’ll find out on your own in hours.

Another good source of free information, as well as assistance if you’re having trouble paying your student loans, is the Student Loan Alliance. You can find them at StudentLoanHelp.org. Finally, you can also turn to our Solutions Center for help with student loans.

What’s your experience with student loans? Share with us in comments below or on our Facebook page.

Got a question you’d like answered?

You can ask a question simply by hitting “reply” to our email newsletter. If you’re not subscribed, fix that right now by clicking here.

The questions I’m likeliest to answer are those that will interest other readers. In other words, don’t ask for super-specific advice that applies only to you. And if I don’t get to your question, promise not to hate me. I do my best, but I get a lot more questions than I have time to answer.

About me

I founded Money Talks News in 1991. I’m a CPA and have also earned licenses in stocks, commodities, options principal, mutual funds, life insurance, securities supervisor and real estate. I’ve been investing in both stocks and property for more than 35 years.

Got some time to kill? You can learn more about me here.

Got more money questions? Browse lots more Ask Stacy answers here.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.