Here’s a question from a reader in an all-too-common position these days: drowning in student loan debt.

Hi, Stacy,

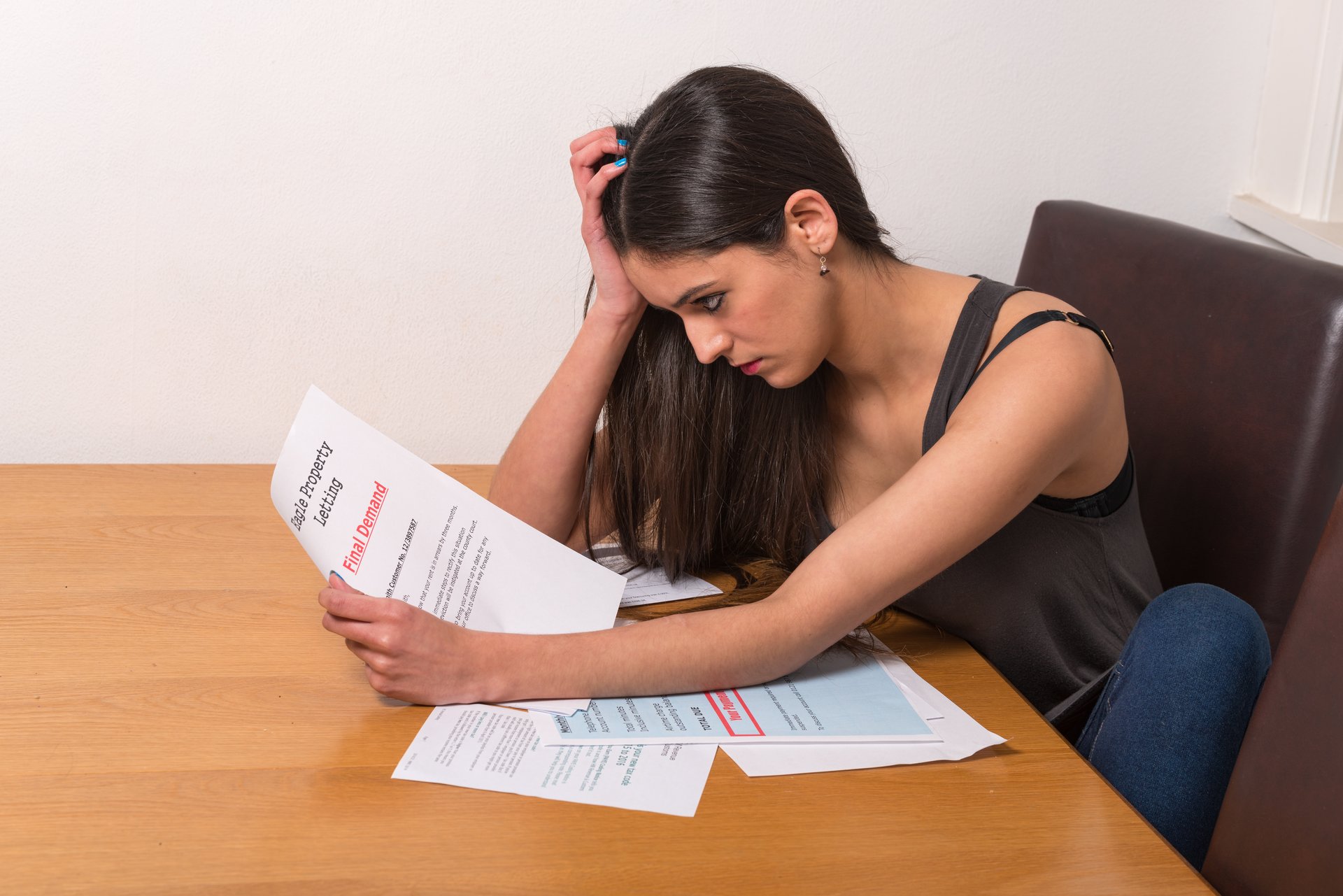

I have a little bit of credit card debt, but it isn’t that bad. What really hurts is all the student loans that I have.Unfortunately for me, I was the first of my siblings to go to college, and so my parents and I were very new to getting financial aid and all of that. I ended up having to pay for almost my entire education with student loans. Now more than half my paycheck goes to paying them off, and I don’t feel like I am making any sort of a dent. I am trying to find the best way to pay them off without going completely broke.

I think my student loan debt is around $126,000 and I have several different companies that I have loans with: The Department of Education, Wells Fargo, AES and ACS. I’ve tried to figure out consolidation on my own, but it is all very confusing. Do you have any tips for me?

I’d appreciate any advice you can offer!

Thanks,

— Becky

I wish Becky’s problem was unique, but she’s definitely got company. Some statistics on the Class of 2015 from a Wall Street Journal article (subscription wall):

- The average debt for 2015 graduates who have student loans was more than $35,000. That’s about twice what it was at the turn of the 21st century.

- More than 70 percent of those getting bachelor’s degree in 2015 had a student loan. Twenty years earlier, fewer than half did.

- According to the Federal Reserve Bank of St. Louis, of those Americans paying down student debt at the end of 2014, more than 27 percent were at least a month behind on their payments.

Guess what? The Class of 2016 racked up an even bigger debt load — more than $37,000 for the average student loan borrower, according to CBS MoneyWatch.

College should improve your life — not ruin it

Before we start on Becky’s question, indulge me while I do a little venting.

While we’re all responsible for the consequences of our actions, I believe part of the blame for the ridiculous level of student loan debt rests with America’s higher education system. College shouldn’t cost so much, and more should be done to educate students and families about avoiding this sort of massive borrowing.

For example, thanks to technology, it’s relatively easy to shave tens of thousands from the cost of college. This post about the growing popularity of online learning, explains how online courses are one way that students can save thousands of dollars on the way to a degree:

[Stuart] Butler, of the Brookings Institute, predicts first-year students will slowly disappear from campuses. Those students now are schools’ cash cows, taking many introductory courses in which hundreds at a time are lectured cost effectively by one professor. When students take more (online courses), perhaps they will delay attending campus until, say, their junior years …

There are many private companies that have found a way to profitably exploit a bloated, radically overpriced higher education system by offering online college courses.

The nation’s universities are developing and expanding online offerings, but they have been slow to join in. Why? Because rather than making education more attainable, the current system is geared to making loans more attainable. Uncle Sam and banks profit on the loans, taxpayers provide the guarantees, and students and their parents are led to believe that massive loans are simply part of the college experience.

In a 2012 article from Bloomberg titled “Student Loans: Debt for Life,” Obama Education Secretary Arne Duncan said, “Obviously if you have no debt that’s maybe the best situation, but this is not bad debt to have. In fact, it’s very good debt to have.”

Tell that to Becky, Mr. Duncan.

Our universities should take some of that massive brain power and refocus it on serving students instead of supporting a system that’s obviously collapsing under its own weight. The high cost of higher education is a national disgrace.

That’s my two cents. Now let’s get to Becky’s question.

Government options for reducing student loans

Contrary to conventional wisdom, the government isn’t entirely heartless. It does offer ways to defer, consolidate or even forgive certain student loans. The catch is you must have loans through the government – private loans aren’t eligible – and you may have to commit yourself to a career in public service.

Here’s what you can get through the government:

Deferment or forbearance: If you’re having trouble making payments, your first course of action should be to contact your loan servicer to ask for a deferment or forbearance. While the details differ slightly, both work by suspending your payments for a period of time.

Deferments can last longer, and the government may even pay your interest during that time. However, you typically need to be unemployed, in the military or in school to get one. Forbearances can be mandatory or discretionary, and discretionary forbearances include the catch-all category of “financial hardship” as a reason for eligibility.

Loan consolidation: Another option to reduce payments may be to consolidate your loans. If you have multiple government loans, you can apply, at no cost, for a consolidation loan. This turns your multiple loans and monthly payments into one loan and one (hopefully lower) payment amount.

However, be aware that while selecting a longer repayment term may lower your monthly payments, it could also increase the overall amount you’re paying on your student loans.

Income-based repayment plans: The standard government repayment plan is 10 years, but that certainly isn’t your only option. Other repayment plans go as long as 20, 25 or, in the case of consolidated loans, 30 years.

There are also several repayment options:

- Income-Based Repayment Plan

- Pay as You Earn Repayment Plan

- Income-Contingent Repayment Plan

- Income-Sensitive Repayment Plan

These plans all have monthly payments tied to your income and can be ideal if you find yourself stuck in a low-wage job. For some programs, you may need a partial hardship to qualify, but after 20 to 25 years of repayment, any remaining debt is forgiven.

Student loan forgiveness programs: Finally, you may be able to have your loan forgiven if you’re a teacher or work in a public service field. However, you need to have the right loans to make this work.

- Public Service Loan Forgiveness: Only those with Direct Loans are eligible for this program, which forgives any remaining debt after 10 years of public service. To qualify, individuals must work for a government or qualifying nonprofit agency and make 120 full and on-time student loan payments while employed in the public service sector.

- Stafford Loan Forgiveness Program for Teachers: The eligibility requirements for this program are a little more complex, but basically you need to teach full-time in a qualifying low-income school for five consecutive years. A similar forgiveness program is offered to those with Perkins Loans.

States might offer their own loan forgiveness programs to teachers, doctors and other professionals as well. You can learn more about federal forgiveness programs and government options on the U.S. Department of Education website. For other programs, check with your state higher education department or agency.

Getting help with student loans

As you can tell from this discussion, the rules governing the various student loan programs can be complex. That, along with the vast number of people needing help, has created a cottage industry in providing paid advice and assistance for student borrowers.

Be careful when dealing with any company offering to help you for a fee. They may charge hundreds of dollars to fill out the same simple forms you could complete and submit yourself for free. Some may outright lie, and at least one state has sued two companies for fraud.

If you do feel so overwhelmed that it is worth it to pay a third party to manage your student loan debt, choose the company carefully. Check with the Better Business Bureau and search for online reviews. Above all, be wary of any company insisting you should stop paying your loans while it negotiates your debt. That is a surefire way to default on your loans, and, trust me, you don’t want to go there.

Third-party companies may also claim to help with private lenders. Again, there is nothing they can do that you can’t do yourself – namely, refinance or try to negotiate a forbearance. Private loans offer little flexibility, which is why, if you haven’t taken out any loans yet, try to stick to federal loan programs.

If you do decide to hire help for student loans, a good place to start is in the Money Talks Student Loan Solution Center. At least there you can feel confident of finding a source that won’t rip you off.

Maryalene LaPonsie contributed to this report.

Got a question you’d like answered?

A great way to get answers to just about any money-related question is to head to our Forums. It’s the place where you can speak your mind, explore topics in-depth and, most important, post questions and get answers. It’s also where I often look for questions to answer in this weekly column. You can also ask questions by replying to our daily emails. If you’re not getting them, fix that right now by subscribing here.

About me

I founded Money Talks News in 1991. I have a CPA, and have also earned licenses in stocks, commodities, options principal, mutual funds, life insurance, securities supervisor and real estate. Got some time to kill? You can learn more about me here.

Got more money questions? Browse lots more Ask Stacy answers here.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.