Most people need a home loan to get the dwelling of their dreams. It is one form of debt that financial experts typically do not frown upon.

However, there are times when it makes sense to pay off your home loan early.

Reducing the time it takes to retire your mortgage may help free up monthly income for other purposes. What follows are examples of when it pays to pay off a mortgage ahead of schedule.

1. You’re tired of paying interest to a lender

Lenders earn money by collecting interest on loans. That means the longer it takes to pay off your home loan, the greater the profit your lender will realize.

If you bought a home using a 30-year, fixed-rate loan, consider trying to pay off the loan in 15 years instead. You’ll probably need to make short-term financial sacrifices to come up with the extra cash, but you’ll save many thousands of dollars in interest costs if you do.

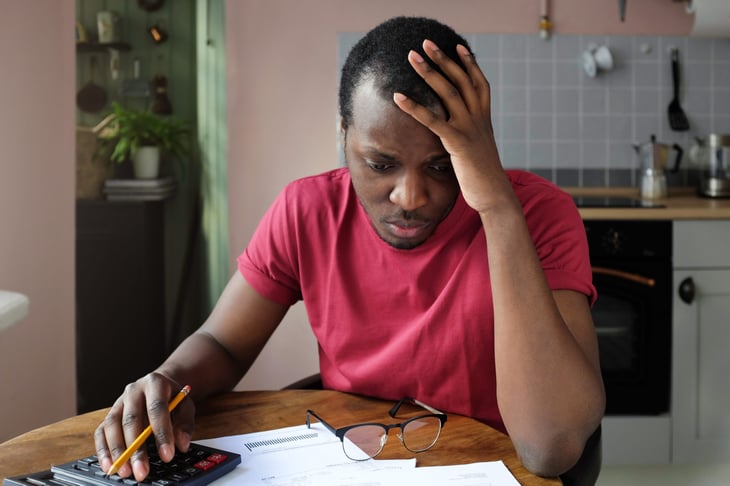

2. The weight of your mortgage payments is causing you stress

Taking on a home loan is a major commitment. It means you must come up with a monthly payment for up to three decades, no matter what other financial challenges you may face.

If you miss payments, your home might go into foreclosure, putting your investment at risk. If worrying about paying the mortgage keeps you up at night, end the agony by coming up with a new payment plan that retires the debt early.

3. You want to free up monthly income for retirement

A home loan typically is the largest single financial obligation people face. Many homeowners strive to pay off their mortgage before reaching retirement age. That way, they can reduce monthly expenses before they quit their jobs and begin living on fixed incomes.

Paying off a 30-year mortgage before retirement can be a challenge. The reward is that you’ll have more disposable income in old age.

If you can’t quite pay off the mortgage at this moment, at least consider getting a home loan with a lower rate. Stop by our Solutions Center to compare your mortgage refinance options.

4. You’re planning to put your kids through college

If you have children who will attend college while you are paying off a home loan, you may face a tough financial burden.

However, paying off your home loan early will give you more flexibility to address college costs.

5. You want to gain access to your home’s full equity

Paying off a home loan early gives you the financial security of having access to your home’s full equity, the market value of your property. That means you’ll have a ready source of cash to address unexpected expenses.

Just remember that tapping into home equity isn’t free. It requires you to take out a loan that will need to be repaid.

6. You want the freedom to explore new opportunities

When you’re making payments on a home, it limits your ability to explore career opportunities. Giving up a dependable, steady job to try a new profession or to return to school can be a risky venture.

If you can pay off a home loan early, you’ll have fewer financial obligations and more freedom to pursue dreams. These might include starting a business or embarking on a new career.

Once your loan is paid off, your monthly expenses will drop and your home will become a financial asset you can draw on.

7. You’re not comfortable carrying a large debt

For people who are averse to debt, owning a home free and clear is a benefit that can’t be measured in dollars and cents.

Holding the title to your own dwelling can bring you a sense of security and peace of mind. You’ll know that even if you suffer a financial setback, the home will be yours. Because residential real estate typically appreciates in value over time, paying off a home loan early is a sound long-term investment.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.