Today I received this question from a reader who’s concerned about Credit Counseling:

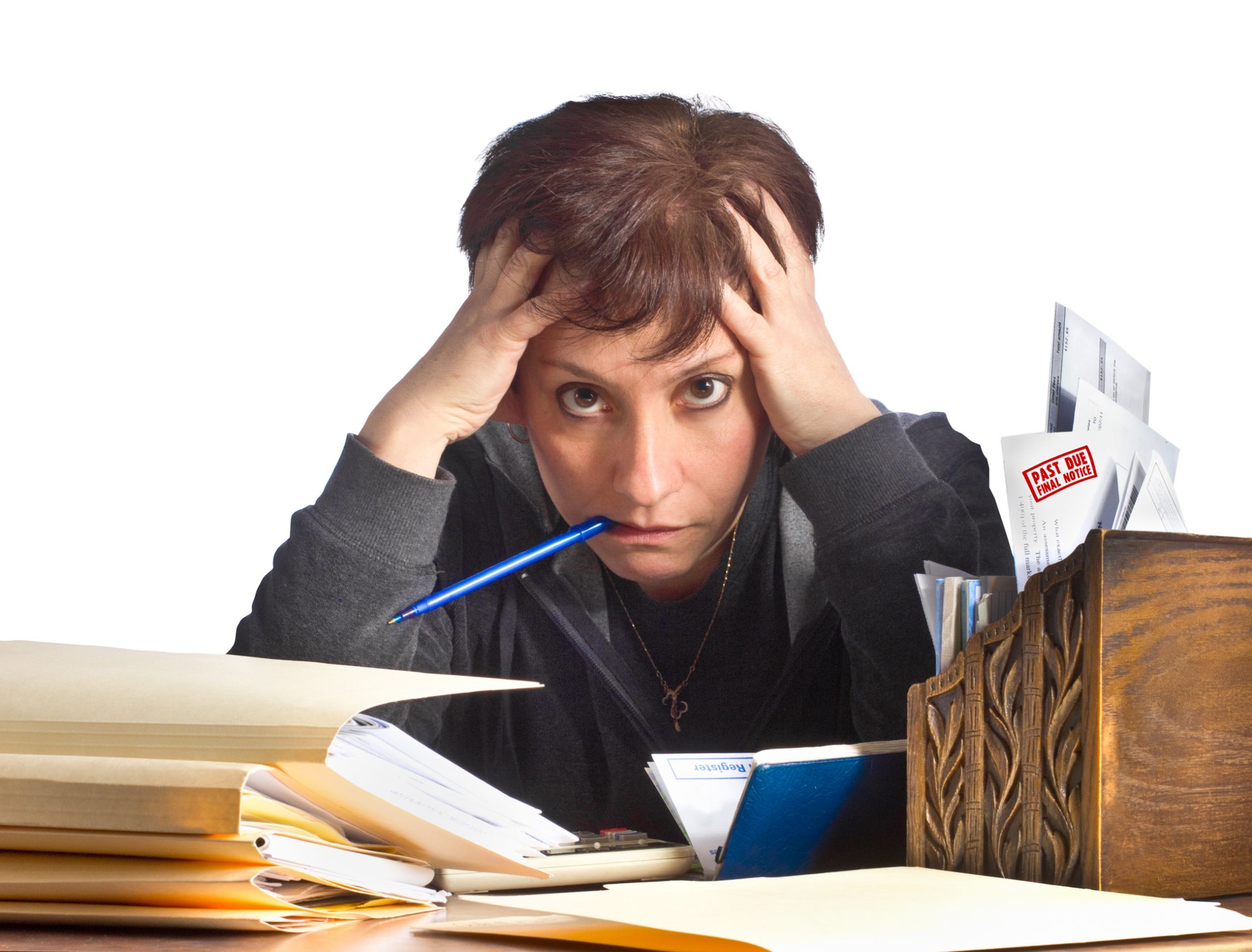

I have been researching the various services and programs you have stated in your article (about credit counseling) which are legitimate and helpful. I just spoke with someone at the Consumer Credit Counseling Service in my area. He immediately suggested I go into a Debt Management Program. With that, he stated that I would have to relinquish ALL of my existing credit cards and any available use of credit. Believe me, I want to get rid of my $40,000 of credit card debt, but stripping away everything at once, how can someone live with that? It seems a bit harsh, for a period of about 5 years….I am 64 years old!!! I have been looking for an agency or org. that belongs to AICCCA [editor’s note: this is a different credit counseling organization: see the credit counseling article]

Can you suggest any? I am really at my wits end with the stress surrounding all of this……don’t know which way to go ……Thanks for your help and guidance, Stacy…. Marisa

Here’s your answer, Marisa:

To find an AICCCA member, you’d go to the AICCCA website However, if you expect to find a different answer there regarding surrendering your credit cards, you won’t.

Part of the process in a debt management program is to relinquish your existing credit cards so you won’t have the ability to rack up more debt while paying off the debt you have. Which to me seems pretty reasonable. So here’s my question to you: if you already owe $40,000 on credit cards that you’re obviously having trouble paying off, why would you want the ability to owe more?

If cigarettes gave you cancer and you were able to find a cure, you should find it pretty easy to give up smoking. You’ve got the financial equivalent: you should it find it pretty easy to give up the cause.

I don’t know how you got into the situation you’re now in: a layoff, an illness, or simply living beyond your means. But whatever the cause, you’ve got to deal with it, and the sooner the better. None of your options are painless, and all will result in varying degrees of hassle, heartache and a limit to your ability to borrow. Let’s review the possibilities.

- Pay it yourself: something you’re obviously having trouble with. You could, however, try to contact your creditors and try to negotiate lower rates, fee waivers, etc, to make your debt more manageable. Not likely, since most banks are notoriously inflexible and difficult to deal with, but theoretically possible.

- Do nothing. Simply stop paying some or all of your debts: you’ll be hounded by collection agencies and probably successfully sued. Your creditors will get a judgment and seize your assets. Whether that matters to you or not depends on whether you have any assets to lose.

- Do the debt management plan you refer to above, which as you point out, will require that you stop using credit cards and make monthly payments for 5 years.

- Try to do a debt settlement plan. Here’s a story I did on that: it’s something I might recommend if you have some cash to settle your debts, but I DO NOT RECOMMEND going to a debt settlement company: that will definitely ruin your credit, and if you end up with the wrong company, you could even be ripped off.

- File bankruptcy: Here’s a story I did on that. This is something you might want to discuss with a lawyer. This will definitely mess your credit up for years to come. You certainly won’t have a credit card in this scenario either, at least not at first. And it may require you surrendering a lot of your net worth: whether these things matter to you will depend on how much money you have to lose and how much you care about your credit.

If you feel any moral obligation to repay the money you borrowed, note that of all the options above, only two accomplish that: paying it yourself and using a debt management plan. Since none of the other options result in repaying your debt in full, all will have a greater negative impact on your credit history and credit score.

So, what should you do? If I were in your situation, my next call would be to a bankruptcy lawyer for a free consultation to learn more about that option. If you don’t like what you hear, and don’t have the money to attempt a debt settlement, I’d probably go with the debt management plan.

Important: As you go forward, I’d advise that you adjust your attitude. A debt management plan has consequences that you accurately label as “harsh.” So do the other options. The solutions are harsh because your situation is harsh. I applaud you for taking the initiative to try to help yourself rather than burying your head in the sand. But get used to the idea that digging yourself out of this mess is going to require mental, financial and emotional sacrifice.

But there’s light at the end of this tunnel. One of my best friends went to CCCS 5 years ago and did a debt management plan. She surrendered her credit cards and paid off her debt over 4 years. Now she’s debt-free and her credit score has radically improved. She could easily get more credit cards; but now she doesn’t want them. She’s learned that a life without plastic is not only possible, it’s better.

24 or 64, we can always learn something new.

Please keep in touch and let me know what you do next and how it works out.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.