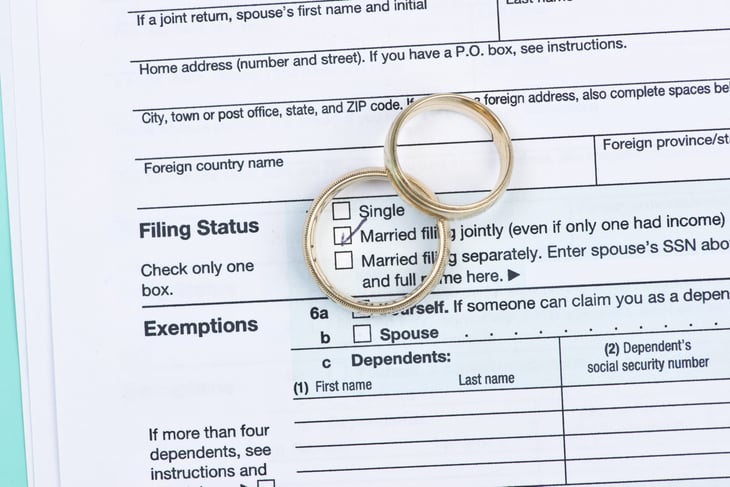

Every tax season, married couples typically must choose how to file their taxes.

If a couple want to use the tax-filing status known as “married filing jointly,” they file a single tax return that reflects both of their income. If they want to use the filing status known as “married filing separately,” each spouse files his or her own return.

While there are situations in which married couples are better off filing separate returns, there are numerous benefits to filing a joint return. Most couples save money by filing jointly. Or, as the IRS plainly puts it, “[Y]ou usually pay more tax on a separate return.”

Read on for some of the top benefits of filing a joint federal income tax return.

The filing requirement threshold is higher

Not everyone is required to file a tax return. It depends on a couple of factors, including your tax-filing status and your gross income.

To determine whether someone is required to file a return, the IRS uses thresholds known as “filing requirements.” The threshold for married couples filing separately is significantly lower than for other tax-filing statuses.

For example, for the 2023 tax year — the one for which returns are due by April 2024 — the threshold for a married couple filing jointly is $29,200 (or slightly more if at least one spouse is age 65 or older). In other words, such a couple doesn’t have to file a 2023 tax return unless their 2023 gross income exceeds $29,200 (or more).

For a married couple filing separately, however, the threshold is much lower: $5.

Medicare surcharges are lower

Medicare is the federal health insurance program for people who are 65 or older or have certain health conditions or disabilities.

The amount of your Medicare premiums depends on your income and tax-filing status. If your income is over a certain threshold, you’ll owe the standard Medicare premium amount as well as a surcharge, known as an income-related monthly adjustment amount (IRMAA).

Take Medicare Part B premiums for 2024 for example: You will be charged an IRMAA if what’s known as your modified adjusted gross income (MAGI) exceeds $206,000 if your tax-filing status is married filing jointly or $103,000 if you use any other filing status.

Say your MAGI is only slightly above those thresholds. Your Part B IRMAA for 2024 will be $69.90 per month (or about $839 per year) — with one exception. IRMAAs are often steeper for married individuals who live with their spouse at any point during a tax year but file a separate tax return. For example, if you live with but file separate taxes from your spouse and your MAGI is slightly more than the $103,000 threshold, your Part B IRMAA for 2024 will be a whopping $384.30 per month (about $4,612 per year).

In short, many married couples can lower their IRMAAs simply by filing their taxes jointly rather than separately.

You can claim the American opportunity credit

If you have a dependent who has yet to complete their first four years of college, you might be eligible to claim the American opportunity credit. This tax credit is worth up to $2,500 per eligible student.

You can forget about this credit if you are married and file a separate return, though. It’s one of several tax breaks that the IRS simply does not allow you to claim if your tax-filing status is married filing separately.

You can claim the lifetime learning credit

The lifetime learning credit is for eligible educational expenses that you incur to improve your job skills or pursue an advanced degree. It’s worth up to $2,000.

Married couples who file separate returns cannot claim the credit. But those who file jointly (or use any other tax-filing status, for that matter) can use this IRS chart to help them determine whether either education credit applies to their tax situation. And don’t forget that if you and your dependent both have educational expenses, you might just qualify for both the American opportunity and lifetime learning credits.

You can deduct student loan interest

Taxpayers who make student loan payments might be eligible to deduct up to $2,500 in interest on their tax return.

If you use the married filing separately status, you won’t qualify for this tax deduction. But if file jointly (or use any other filing status), use this IRS tool to determine if you can deduct your student loan interest.

If you are eligible to deduct it, be sure to get a Form 1098-E from your lender if you paid $600 or more in interest. This tax form contains information that you must enter on your tax return in order to deduct your interest.

It’s easier to claim the credit for the elderly or disabled

This tax credit could be worth up to $7,500 if you are 65 or older or are on permanent and total disability and if you otherwise qualify for the credit. (Use this table and flow chart in IRS Publication 524 to see if you qualify.)

It’s harder to qualify if your tax-filing status is married filing separately, though. For example, if you lived with your spouse at any point during the tax season but file separately, you can’t claim the credit for the elderly or disabled at all.

It’s easier to claim the earned income tax credit

The earned income tax credit is for workers with low to moderate incomes. For taxpayers who qualify for the credit for the 2023 tax year, it’s worth up to $600 if they have no qualifying children or up to $3,995 to $7,430 if they have one or more qualifying children. (You can use this IRS tool to see if you are eligible.)

One exception is for taxpayers who use the filing status of married filing separately and have no qualifying children: They are not eligible to claim the earned income tax credit at all. But if you file jointly (or use any other filing status), you can claim the credit even without any qualifying children, as long as you otherwise meet the requirements of the credit.

It’s easier to claim the child and dependent care credit

The child and dependent care credit is for expenses related to the care of your dependent while you’re at work or looking for work.

Depending on your adjusted gross income, this credit could be worth anywhere from 20% to 35% of the qualified amount you spent on dependent care. That amount is capped at $3,000 if you pay for care for one qualifying dependent and $6,000 for two.

It’s harder to qualify for the credit if your filing status is married filing separately; in that case, you might qualify only if you’re legally separated or living apart from your spouse. If that’s you or if you file jointly (or use any other filing status), you can use this IRS tool to determine if you’re eligible for the credit.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.