The best Roth IRAs let workers save after-tax dollars for retirement without paying exorbitant fees. However, it can be hard to choose a provider when so many companies offer Roth IRA accounts with competing deals.

To help you meet your retirement goals, we’ve compared the top Roth IRAs available today based on factors such as investment options, educational resources, fees, and minimum account investment/balance requirements.

The Roth IRA providers we’ve highlighted below stand out from their peers, thanks to their low ongoing costs and a broad selection of investment options, as well as the ease with which you can open an account.

Our top picks for best Roth IRA accounts

- Fidelity Investments: Best overall

- Charles Schwab: Best investment options

- Merrill Edge: Best bonus offer

- E-Trade: Best for low trading fees

- Vanguard: Best for mutual funds

- Betterment: Best robo-advisor option

- Ally Invest: Best by an online bank

- Interactive Brokers: Best for active traders

Best Roth IRA reviews

Fidelity Investments: Best overall

Highlights:

- No annual account fees

- No minimum balance requirements for open accounts

- $0 commissions for online U.S. stock, ETF and options trades

- Wide selection of mutual funds, stocks, bonds, ETFs, CDs and more

Fidelity Investments offers a smart Roth IRA option with no annual account fees, no required minimum balance, and wide selection of investment options.

The company also offers tools like an IRA Contribution Calculator and educational resources to help prepare you for retirement. You’ll also get Fidelity’s intuitive online interface that makes it easy to research and track your investments over time.

Note that, in addition to not charging annual account fees, Fidelity also offers $0 commissions for online U.S. stock, exchange-traded funds (ETFs) and options trades.

Charles Schwab: Best investment options

Highlights:

- No minimum balance requirement to open an account

- No annual account management fees

- Access to stocks, CDs, bonds, ETFs and more

- Free ETF trades online within your Schwab account

- Stock “slices” cost as little as $5

- Merger with TD Ameritrade underway

Charles Schwab is another leading brokerage firm that now makes it easy to open a Roth IRA online, as there are no minimum account deposits required, and you won’t pay any annual account maintenance fees.

Schwab also has made investing a lot more accessible to small investors with Schwab Stock Slices. With this service, you can buy a fraction, or slice, of any stock in the S&P 500 for as little as $5. Purchase a single slice or as many slices as you want up to a maximum of $50,000 per transaction.

You’re not limited to investing in one company either – buy slices in a single company or up to 30 different ones — with no commissions for online purchases.

You get access to retirement planning tools and resources such as the company’s robo-advisor Schwab Intelligent Portfolios — automated investing with 24/7 live support without advisory fees or commissions — and in-person help at more than 300 Charles Schwab locations nationwide.

Merrill Edge: Best bonus offer

Highlights:

- No minimum balance requirements for self-directed Roth IRA accounts

- A wide range of stocks, options, bonds, ETFs and well-known mutual funds

- $0 online equity and ETF trades

- Up to $600 cash bonus for opening a Roth IRA account

- Easy sync with Bank of America accounts

Merrill Edge received high marks in our analysis thanks to its low fees, wide investment selection and generous inscription bonus. There are restrictions to this last offer, however: You have to make a qualifying deposit to your new account within 45 days, and you must keep that qualifying deposit intact for 90 days.

Though there are no account fees for online stock and ETF trades, options trades carry a per-contract fee of 65 cents.

If you bank with Bank of America, you’ll have a seamless experience adding a Merrill Edge brokerage account and transferring funds up to the IRS’ annual contribution limit.

E-Trade: Best for low trading fees

Highlights:

- No minimum balance requirements

- $0 commissions for online stock, ETF and options trades

- Access to over 4,500 no-load mutual funds with no transaction fees

- Access to live market data and analysis using E-Trade’s online platform

- E-Trade is now part of Morgan Stanley

E-Trade made our list of best Roth IRA accounts thanks to its low trading fees, which can be especially attractive to active investors. Fees for mutual funds can vary, but E-Trade does give you access to over 4,500 mutual funds with no loads and no transaction fees. Options start at 50 cents per contract, and futures are $1.50 per contract.

There are no minimum account balances required for this account either, and E-Trade’s online trading platform makes it easy to access live market data and analysis.

E-Trade also has a large library of educational resources and tools, including a “Knowledge” section that breaks down the basics of investing, while also giving advice on advanced trading and tax planning.

E-Trade was acquired by bank Morgan Stanley on Oct. 2, 2020. As of April 2021, there haven’t been any changes in E-Trade’s pricing and offerings.

Vanguard: Best for mutual funds

Highlights:

- Low expense ratios and fees

- Large selections of mutual funds, ETFs and other investment options

- No sales loads or commissions

With more than 200 commission-free ETFs and mutual funds to choose from, and a history of zero to low fees, Vanguard can be an excellent Roth IRA option.

The expense ratios on Vanguard funds are 0.10%, among the lowest in the industry, meaning you’re not going to have high fees eating into your profits. The company’s mutual funds also have no sales loads, sales commissions, or account service fees if you choose to receive your account documents electronically.

You can also choose how to pick your investments – either select targeted funds with a diversity of investments, pick and choose different funds to create a custom portfolio, or get expert help from one of Vanguard’s agents.

Betterment: Best robo-advisor option for beginners

Highlights:

- 0.25% annual fee (pricing increases to 0.4% of account for Premium Account)

- Intuitive set-up and asset allocation

- No minimum deposit required to start

- Betterment now has its own high-yield savings account

- Can link up to other, external accounts

- Easy-to-use smartphone app

Opening a Roth IRA through Betterment is a great way for beginners to start a retirement plan on their own without a minimum deposit.

You’ll also get automatic rebalancing to optimize the growth potential of your retirement savings. Betterment charges an annual fee of 0.25% of your account.

The biggest drawback is the lack of investment advice from an in-person financial advisor or certified financial planner. Another drawback for some retirement savers is the reliance on ETFs. Betterment’s portfolios won’t include individual stocks.

Ally Invest: Best by an online bank

Highlights:

- Easy to set up and fund online

- No account minimum deposit to begin

- Strong educational resources

- Connected high-yield savings account

- Top-notch trading dashboard with real time data

- Tax benefits are easy to track on Ally’s online dashboard

With Ally, investors can open a Roth IRA without a minimum balance requirement and fund the account easily by linking to any other bank or credit union. The company offers commission-free trading on individual stocks and thousands of ETFs. Like many platforms, Ally charges a contract fee for options trading (50 cents per trade).

Since it’s connected to an online-only bank, Ally Invest excels with its online tools and educational content. In a way, Ally Invest resembles a robo-advisor but it attracts active traders with its easy-to-use interface and wide variety of securities.

Interactive Brokers: Best for active traders

Highlights:

- Investment products based on customer demand

- Online brokers can invest globally

- $0.005 charge per share with interactive brokers

- Over 8,300 no-transaction-fee mutual funds available

If you want to actively invest with your Roth IRA, then Interactive Brokers‘ IBKR Pro is your best bet. Not only will the company provide investment products based on their own customer demand, but it also opens up the option to invest in the global market. Additionally, all Interactive Brokers IRAs have no opening or closing fees, and there are no opening amount requirements.

When trading stocks with an IBKR Pro account, Interactive Brokers charges $0.005 per share, with a minimum of $1 and a maximum of 1% per trade value. This is among the best fees that we found, but it does come with a disadvantage, which is its strong inactivity fees.

Accounts with balances of $1 million or lower must reach $10 a month in trade commissions; otherwise, Interactive Brokers will charge you the difference per month. However, if you’re 25 or younger, the minimum monthly trade commission decreases to $3. For account balances of $2,000 or less, the minimum trade commission is $20.

Other companies we considered

Wealthfront

Wealthfront’s best features are its low 0.25% management fee, and its robo-advisor capabilities. However, we ended up choosing Betterment for the position of best robo-advisor, due to Wealthfront’s $500 opening deposit and account minimum requirements. This restriction might not be a dealbreaker for some, but it can become an obstacle if you are financially strained.

TD Ameritrade

We considered Ameritrade as the best overall option, thanks to its no-account minimum and $0 commission fees for online stocks. However, it lost this position to Fidelity Investment, as they also have these options, while offering a plethora of low-cost investment alternatives.

SoFi

Although SoFi has robo-advisor capabilities and great customer support, it falls short due to its $75 full outgoing transfer fee, and for not offering tax-loss harvesting or stop-loss orders with their accounts.

M1 Finance

M1 Finance offers strong automated investment services, including flexible customization that adjusts to your investing needs. However, we decided not to pick it as one of our Roth IRA options due to its restrictions. The account has a $500 opening minimum, and you are charged a fee if you have less than $20 in your account and/or if you don’t trade for 90 days.

Fundrise

Fundrise is a solid option if you want to venture into real estate investment. However, we didn’t pick the company because its investment minimums are among the highest.

A starter portfolio needs a $500 minimum investment, a basic plan requires $1,000, and the premium account level requires $100,000. Additionally, since the company focuses solely on real estate, there are some extra fees that can apply, including development and liquidation fees.

Ellevest

Ellevest didn’t make the cut because, even though it has three plans — Essential, Plus and Executive — only the latter two can be used to open IRAs. Additionally, all their plans require you to pay a monthly account management fee, which might not be everyone’s cup of tea. Finally, the company doesn’t provide tax-loss harvesting for their plans.

You Invest

We decided not to include JPMorgan’s You Invest account on our list because of its substantial $2,500 minimum to use the Portfolio Builder tool. Additionally, the company’s investment research offerings are fewer than other companies on this list.

Roth IRA guide

What is a Roth IRA?

Unlike tax-deferred retirement accounts such as a traditional 401(k) or IRA, a Roth individual retirement account, or simply, Roth IRA, requires that you contribute after-tax dollars. While this means you’ll take a tax hit on what you invest now, these accounts do have a trick up their sleeve. With a Roth IRA, your money will grow tax-free until you’re ready to take distributions after age 59½.

When considering whether to open a Roth IRA, take into account the following factors:

- Management fees and expense ratios are often the biggest determinants of your investment returns, since they chip away at your earnings yearly.

- The best Roth IRA providers typically have a robust online presence, and they should make it easy to open your account online.

- Make sure you know the income requirements to contribute to a Roth IRA, which we’ll detail in the next segment.

Both Roth IRAs and traditional IRAs will provide tax advantages. However, when you get to enjoy those advantages will be different. Be sure to compare both options before deciding which is best for you.

Roth IRA limits

You have to meet specific income requirements to contribute to a Roth IRA, and you’ll also face a maximum contribution limit that varies based on your age.

Roth IRA contribution limits

Roth IRA contribution limits are the same for 2021 as they were for 2020, with consumers who earn a taxable income allowed to contribute up to $6,000 across their IRA accounts. For workers ages 50 and older, an additional $1,000 can be contributed for a total of $7,000 per year.

Roth IRA income limits

Keep in mind that not everyone can contribute to a Roth IRA — at least not the full amount. In 2021, married filings with a modified adjustable gross income (MAGI) below $198,000 can contribute the full amount to a Roth IRA.

For couples with incomes between $198,000 and $207,999, the contribution maximum is lowered, while no contributions are allowed at incomes of $208,000 or above.

Single filers or married couples filing separately with a MAGI below $125,000 can contribute the maximum to a Roth IRA in 2021. For incomes between $125,000 and $139,999, contribution limits are lowered, while no contributions are allowed at incomes of $140,000 and above.

Roth vs. traditional IRAs

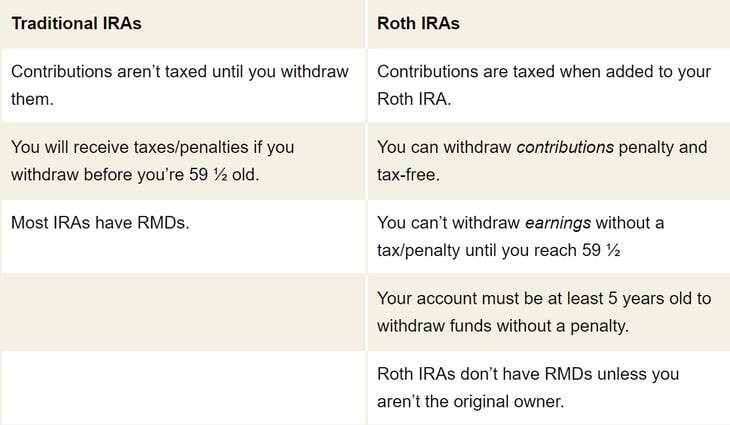

The biggest differences between Traditional and Roth IRAs are the way the accounts are taxed, and when you can withdraw your funds.

Traditional IRAs use pre-taxed money, so your contributions aren’t charged until you withdraw them. When you do, you’re charged income tax on each withdrawal you make.

Additionally, there are some withdrawal rules you must follow with traditional IRAs to avoid fees and/or penalties. You can’t touch the money you contribute until you’re 59½ years old, or else you’ll be charged a 10% early withdrawal penalty.

Most traditional IRAs also have a required minimum distribution (RMD) amount that you must withdraw on a yearly basis after reaching 70½. The RMD amount varies greatly from individual to individual, and is calculated using your age and account balance.

In contrast, with Roth IRAs, you can withdraw your contributions at any time and age — tax- and penalty-free — as long as you’ve had the account open for five years. This is known as the five-year rule.

However, if you aren’t 59½ years old and you withdraw from any earnings your contributions have made, this can trigger income taxes and a 10% penalty.

Finally, Roth IRAs don’t have required minimum distributions (RMDs) unless you’re not the original account owner.

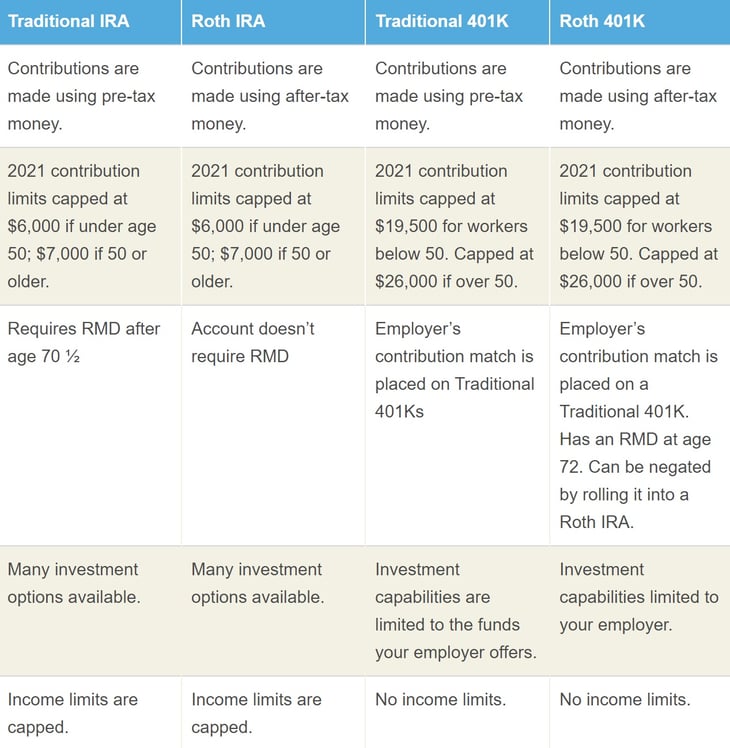

Traditional IRA vs. Roth IRA vs. traditional 401(k) vs. Roth 401(k)

The following chart breaks down the similarities and differences between traditional and Roth IRAs, as well as traditional and Roth 401(k)s.

FAQs

What is a Roth IRA?

A Roth IRA, similarly to a traditional IRA, is an individual retirement account. However, unlike traditional IRAs, Roth IRAs offer tax-free withdrawals in retirement. If you’ve had your account for a minimum of five years, and you’re 59½ or older, you can withdraw at any time without paying federal taxes.

How to open a Roth IRA?

Almost anyone can open a Roth IRA account, as long as they have earned income throughout the year.

You must first check if your total income is eligible to open and maintain an IRA. In 2021, your ability to add to your Roth IRA begins to phase out from $125,000-$140,000.

Next, you should research online for potential providers; you can check our top choices if you want a head start.

Finally, once the paperwork is done, you can then choose how to invest the money that goes to your Roth IRA. You can either design your own portfolio, choose one designed by the investment company, or hire a financial planner to help you pick the best investments and financial goals for your Roth IRA.

How does a Roth IRA work?

Just like traditional IRAs, a Roth IRA is an individual retirement account you can set up to grow your finances over the years.

However, Roth IRAs differ in that the money you invest is taxed when it goes into your account, and not when you withdraw it. This means that the money in your account is tax-free, so you can withdraw it whenever without additional penalties or fees.

How much can you contribute to a Roth IRA?

In 2021, the maximum you can contribute to one or all of your IRA accounts is $6,000 a year if you’re 49 or younger. If you’re 50 or over, you can contribute up to $7,000 yearly.

When can you withdraw from a Roth IRA?

You can technically withdraw your Roth IRA contributions whenever you prefer, as the account doesn’t adhere to the traditional required minimum distribution (RMD) rule. These funds are tax-free, since you’ve already paid taxes on them when you added them to your account.

However, no matter your age, Roth IRAs have a five-year waiting period before you can withdraw any earnings without taxes and/or penalties.

What is the five-year rule for Roth IRAs?

The five-year rule for Roth IRA accounts is a waiting period set to limit your withdrawal of Roth IRA tax-subsidized earnings. Although you can withdraw contributions from your account tax-free and at any time, you can’t do the same with your account’s earnings.

If you withdraw from your earnings before age 59½, and before five years have passed after your account being opened, those funds will be taxed. Additionally, even if you’re 59½, the five-year rule still applies: You must wait five years after opening your Roth IRA if you want to withdraw your earnings tax-free.

How we chose the best Roth IRA accounts

There are numerous companies that offer financial planning via Roth IRA accounts, but they’re not all the same. The providers that made our list came out ahead of the pack based on four important factors: low minimum deposit requirements, low fees, access to low-cost investment options, and account management options.

Low minimum deposit requirements

We only chose Roth IRA accounts with reasonable minimum account opening requirements (or none at all) for this list. This factor is crucial, since many consumers may not have the $1,000 or more to get started and need to invest small sums of money at first.

Accounts with reasonable minimum deposit requirements lower the entry barrier and make it considerably easier for new investors to get into the game.

Low fees

We also looked for Roth IRA providers that offered no account management fees, and had a good variety of no-load mutual funds and low expense ratios. These fees can directly chip away at your investment returns without providing you with any real benefit, so you’re better off not paying them for a self-directed account.

Access to low-cost investment options

All of the Roth IRA accounts that made our list let you choose from a broad range of investment options, many of which can be traded without any fees. We gave preference to financial institutions that offered their own selection of no-fee investment options, whether that includes ETFs, index funds or mutual funds.

Account management options

Finally, we definitely gave preference to Roth IRA accounts with helpful online account management options, including setting up a rollover into another account if you choose.

This includes not only investing tools and resources, but also access to a mobile app that lets you manage and oversee your personal finance accounts on the go.

A few of the Roth IRA providers on our list also offer local branches where consumers can get in-person help, and we consider that a major plus.

Summary of Money’s best Roth IRA accounts of 2021

- Fidelity Investments: Best overall

- Charles Schwab: Best investment options

- Merrill Edge: Best bonus offer

- E-Trade: Best for low trading fees

- Vanguard: Best for mutual funds

- Betterment: Best robo-advisor option

- Ally Invest: Best by an online bank

- Interactive Brokers: Best for active traders

© Copyright 2020 Ad Practitioners, LLC. All Rights Reserved.

This article originally appeared on Money.com and may contain affiliate links for which Money receives compensation. Opinions expressed in this article are the author’s alone, not those of a third-party entity, and have not been reviewed, approved, or otherwise endorsed. Offers may be subject to change without notice. For more information, read Money’s full disclaimer.

Add a Comment

Our Policy: We welcome relevant and respectful comments in order to foster healthy and informative discussions. All other comments may be removed. Comments with links are automatically held for moderation.